Not-So-Stranded Assets

The economic and geopolitical poverty of ESG

The world scrambles for oil, gas, and coal. With inflation, prices soar. Consumers struggle to keep up. Hydrocarbon energy firms, meanwhile, enjoy giant bumps in profits and stock market value.

If you took the advice of the world’s largest financial firm, however, you were ill-prepared for these events. Over the last half-decade, BlackRock, the index fund behemoth, told nations, firms, and investors to pursue so-called green energy and shun hydrocarbons. Now, the nations, firms, and investors who took (submitted to) BlackRock’s advice (diktats) are worse off. They suffer with unreliable and expensive energy mixes, are stuck with bad green investments, and lose out on profitable hydrocarbon investments.

This is environmental, social, and governance investing, or ESG.

Over the last several years, BlackRock and its closest index rivals, Vanguard and State Street, have leveraged their $20 trillion in other-people’s-money to transform capital markets and much more. In a series of annual letters to CEOs and clients, BlackRock CEO Larry Fink argued for “a fundamental reshaping of finance” based on ESG and “stakeholder capitalism.” (See 2019, 2020, 2021, 2022.)

Shareholders We Win, Stakeholders You Lose

Replacing shareholders with hand-picked ‘stakeholders’ is more radical than it sounds. Too often, favored activist ‘stakeholders’ end up running companies, while shareholders and disfavored would-be stakeholders are ignored. ESG not only expropriates the key functions of markets – ownership, capital allocation, price discovery – but it also replaces public decision-making and accountability, or politics. Surreptitiously, it thus undermines two foundations of modern prosperity – democracy and capitalism.

Last summer, we warned in the Wall Street Journal that energy policy was being hijacked. BlackRock and other large financial firms were muscling governments and companies away from sound energy strategies and into fashionable ones, such as windmills and solar, which also happen to be erratic and expensive. The great Texas windmill freeze of January 2021 showed what happens when we over-rely on unreliable technologies.

Some large clients embrace BlackRock’s “fundamental reshaping of finance” because it aligns with their politics. Think CalPERS, the California Public Employees’ Retirement System. For them, ESG is an easy sell. In fact, CalPERS probably sold it to BlackRock in the first place.

Other clients and companies, however, are increasingly wary of ESG stakeholderism. They think it reduces investment choice and makes the world poorer, more volatile, and less resilient.

To these more skeptical clients, BlackRock insists it is merely anticipating the ‘net-zero transition’ to renewable energy and helping firms and investors avoid ‘stranded assets.’ It’s their fiduciary duty, they say, to reduce clients’ exposure to fossil fuels, beachfront real estate, and unwoke businesses. Anticipating big and small shifts in technology, policy, and climate, however, is the job of millions of investors arguing in dynamic markets. So is avoiding or betting on particular assets, stranded or otherwise.

Sensing discomfort and a growing backlash, BlackRock recently boasted that it allows large institutional clients to vote their own proxies. How generous. Millions of retail clients aren’t so lucky – BlackRock votes their shares for them. Regardless, proxy votes for corporate directors and policies are just a fraction of what matters. Collaborating with a vast web of activist consultants, NGOs, and government agencies (see the SEC’s proposed new rules), index funds, commercial banks, and even central banks increasingly exercise a broad spectrum of soft power, seeking to decapitalize industries and firms they don’t like, and pump up those they do. S&P now bases its credit ratings for states not solely on their fiscal outlooks but in part on their allegiance to ESG.

In March of this year, Fink insisted, “You have to force behaviors, and at BlackRock we are forcing behaviors.” BlackRock isn’t passively anticipating the future. It’s actively shaping it.

Inflation Miss

How is BlackRock’s vision working out?

For starters, those stranded assets they told you to avoid have skyrocketed in value, while ESG vehicles struggle. Over the last six months, for example, Exxon Mobil (XOM) shares rose 63% while a key ESG fund (SUSA) dropped 15%. Vanguard’s VDE energy index is way up. Coal profits and shares are exploding, as Bloomberg explains:

Glencore Plc is getting rich on coal. The company is on course for another year of bumper profits, its shares just hit a record high — a feat that looked unlikely for most of the last decade — and investors are set for a windfall of returns.

These gains and losses aren’t permanent. Trends reverse, markets surprise. But that’s the point! BlackRock’s presumption that a large and growing list of assets are off limits and only go one way is anti-fiduciary. It artificially limits the universe of investable vehicles, reducing diversification. ESG leaves investors unprepared for monetary, geopolitical, or technological events which dramatically affect asset prices. If you shunned traditional energy assets, this inflation has hit you particularly hard.

ESG also constrains the decisions and performance of individual companies. Energy firms especially are experiencing a serious case of vertigo. On one hand, the ESG anti-industrial complex orders them to reduce production on the way to one day winding down their operations. On the other hand, politicians around the world panic over exploding gas prices and demand more output.

Drill, Baby, Drill

In his Los Angeles speech on Friday, President Biden railed against Exxon for not producing more oil:

Why don’t you tell them what Exxon’s profits were this quarter?…They’re not drilling. Why aren’t they drilling? Cause they make more money not producing more oil. Exxon, start investing….1

Exactly one year ago, however, BlackRock collaborated with anti-energy activists to place three new directors on Exxon’s board. The new board then voted to reduce output over coming years. As the New York Times explained on June 9, 2021:

Wall Street has seen its share of strange bedfellows, but a recent alliance of investors that took on Exxon Mobil was unprecedented.

Last week, an activist investor successfully waged a battle to install three directors on the board of Exxon with the goal of pushing the energy giant to reduce its carbon footprint. The investor, a hedge fund called Engine No. 1, was virtually unknown before the fight.

The tiny firm wouldn’t have had a chance were it not for an unusual twist: the support of some of Exxon’s biggest institutional investors. BlackRock, Vanguard and State Street voted against Exxon’s leadership and gave Engine No. 1 powerful support.

Mike Wirth, CEO of Chevron, is also confused. In a recent TV interview, he emphasized the massive long-term investments required to supply energy to the globe but questioned whether those can happen “in a policy environment where governments around the world are saying, 'we don't want these products to be used in the future.' And so there really is a dilemma. We receive mixed signals in these policy discussions.”2

The Elephant in the Barrel

Sixteen years ago, we enthused, once again in the Wall Street Journal, about a coming boom in hydrocarbon energy.3 In August of 2006, the high-price panic was about ‘peak oil’ – an imminent and permanent decline in fossil output. Hydrocarbons were tapped out, and we needed a green energy revolution. Remember Solyndra? I said just the opposite: shale fracking would create a hydrocarbon boom and prices would stabilize or fall.

The U.S. pursued this strategy and enjoyed an energy renaissance. Europe did not. ESG came along and reinforced all of Europe’s worst policy instincts, leaving the continent much weaker economically and geopolitically.

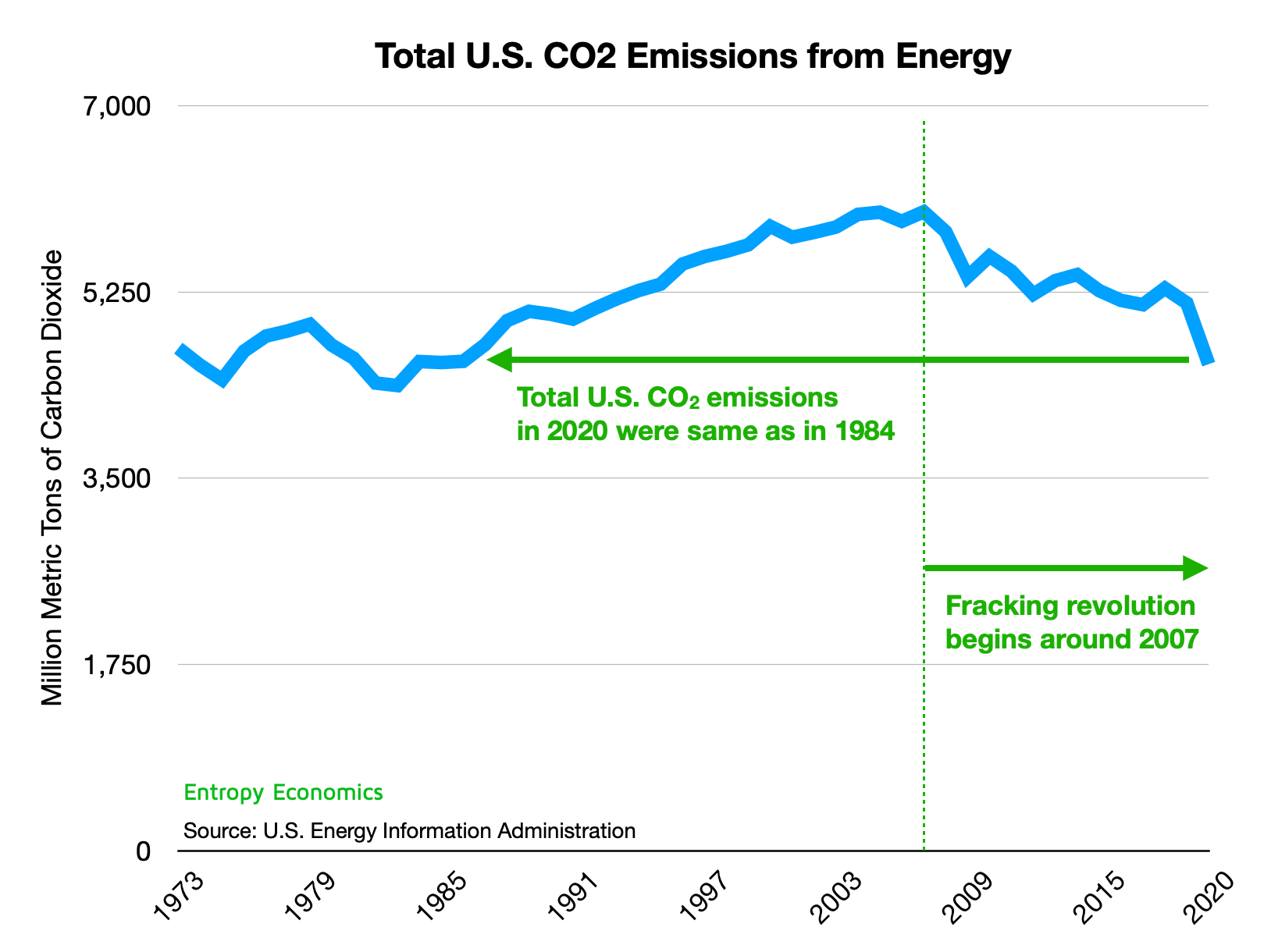

The American fracking revolution didn’t merely reinstate the U.S. as world energy colossus. Because newly abundant and cheap natural gas replaced so much coal, it also dramatically reduced CO2 emissions. Today, despite a vastly larger economy and population, the U.S. emits less CO2 than any time since the early 1980s. This is supposedly the goal of international climate agreements and of ESG. But lower emissions don’t seem to count if they are not achieved via inefficient, fashionable energy sources.

As we know, fashions turn on a dime. For years, Tesla (TSLA) was a green energy hero, the key to keeping fossil fuels underground. Then this spring CEO Elon Musk began loudly criticizing incompetent politicians and censorious social media. He dropped a bomb by acquiring Twitter (TWTR). Then he criticized ESG as a “scam” and the “devil incarnate.”

Suddenly, Tesla’s world leadership in electric vehicles and solar panels was beside the point. S&P Dow Jones kicked Tesla out of its ESG index, demonstrating what ESG is really about – politics and power.

Here is a longer version of President Biden’s June 10, 2022, statement: “We are going to make sure everyone knows Exxon’s profits. Why don’t you tell them what Exxon’s profits were this quarter? Exxon made more money than God this year and by the way, nothing’s changed. One thing I want to say about the oil companies, talk about how they have 9,000 permits to drill. They’re not drilling. Why aren’t they drilling? Cause they make more money not producing more oil. The price goes up number one and number two, the reason they’re not drilling, is they are buying back their own stock, which should be taxed quite frankly, buying back their own stock, and making no new investments. So ugh, I always thought Republicans were for investment. Exxon start investing and start paying your taxes, thanks.”

In a 2020 presidential debate, President Biden insisted on a very different policy: “No drilling, period.”

Here is Wirth’s longer statement: “We've seen refineries closed. When I began my career, there were more than 250 refineries in the US. Today there's half that number and we've seen refineries close around the world.

“It puts the industry in a difficult spot because building a refinery is a multi-billion dollar investment. It may take a decade. We haven't had a refinery built in the United States since the 1970s. My personal view is, there will never be another refinery built in the United States, but you're looking at committing capital ten years out that will need decades in which to offer a return to our shareholders. In a policy environment where governments around the world are saying, 'we don't want these products to be used in the future.' And so there really is a dilemma.

“We receive mixed signals in these policy discussions, and my message would be we need to sit down and have an honest conversation, a pragmatic and balanced conversation about the relationship between energy and economic prosperity, national security and environmental protection. We need to recognize that all of those matter – and we can't over index on just one.”

Bret Swanson. The Elephant in the Barrel. The Wall Street Journal. August 12, 2006.